Deep Cycle Battery Market Market Growth and Trends:

The deep cycle battery market is undergoing significant transformation as technological advancements, shifting consumer preferences, and evolving regulatory landscapes drive changes in the industry. Understanding the latest trends and insights is crucial for stakeholders seeking to navigate this dynamic market and capitalize on emerging opportunities. The deep cycle battery market is estimated to be valued at USD 2.57 billion in 2024 and is expected to reach USD 4.32 billion by 2031, growing at a compound annual growth rate (CAGR) of 7.2% from 2024 to 2031. One of the most notable trends in the Deep Cycle Battery Market Demand is the increasing adoption of lithium-ion technology. Lithium-ion batteries offer higher energy density, longer cycle life, and faster charging capabilities compared to traditional lead-acid batteries, making them well-suited for a wide range of applications. As a result, lithium-ion batteries are gaining traction in sectors such as electric vehicles, renewable energy storage, and portable electronics, driving growth and innovation in the deep cycle battery market. Another key trend is the growing emphasis on sustainability and environmental responsibility. With concerns about climate change and resource depletion on the rise, there is a growing demand for eco-friendly battery solutions that minimize environmental impact. Manufacturers are increasingly investing in research and development efforts to develop greener battery chemistries, improve recycling processes, and reduce the carbon footprint of battery production and disposal. Furthermore, advancements in battery management systems (BMS) and smart grid technologies are reshaping the way deep cycle batteries are utilized and managed. BMS technologies enable real-time monitoring and optimization of battery performance, maximizing efficiency, and prolonging battery life. Smart grid technologies facilitate the integration of deep cycle batteries into energy systems, enabling dynamic energy management, grid stabilization, and demand response capabilities. Trends and Insights: One of the emerging trends in the deep cycle battery market is the convergence of energy storage and digital technologies. As the Internet of Things (IoT) and artificial intelligence (AI) continue to proliferate, deep cycle batteries are becoming increasingly intelligent and interconnected. Smart batteries equipped with sensors and IoT connectivity can monitor performance metrics, detect anomalies, and optimize charging and discharging processes in real-time, enhancing reliability and efficiency. Another trend to watch is the increasing demand for modular and scalable battery solutions. With the rise of distributed energy resources and microgrid applications, there is a growing need for flexible and adaptable energy storage systems that can be easily scaled up or down to meet changing demand and accommodate future expansion. Modular deep cycle battery systems offer the flexibility and versatility needed to address these evolving requirements, making them a preferred choice for a wide range of applications. Additionally, the deep cycle battery market is witnessing a shift towards vertical integration and partnerships across the value chain. Battery manufacturers are forming strategic alliances with suppliers, distributors, and end-users to streamline operations, reduce costs, and gain a competitive edge in the market. By leveraging complementary strengths and resources, companies can enhance their product offerings, expand their market reach, and drive innovation in the deep cycle battery market. The deep cycle battery market is experiencing rapid evolution and transformation, driven by technological advancements, changing consumer preferences, and regulatory developments. By staying abreast of the latest trends and insights, stakeholders can position themselves for success in this dynamic and highly competitive market, driving growth, innovation, and sustainability in the years to come.

0 Comments

Enterprise Search Market The enterprise search market provides search capabilities within organizations to search through internal data repositories including file servers, intranets, document management systems and enterprise resource planning applications. It allows employees to find organizational information and assets like documents, emails and people much faster, helping improve decision making. The global enterprise involves complex software solutions deployed on-premises or offered as SaaS. It analyzes structured and unstructured data from various internal sources to deliver relevant search results.

The market size for enterprise search is estimated to be valued at US$ 6564.18 Mn in 2024 and is expected to exhibit a CAGR of 14% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the enterprise search market are Abbott Laboratories, QIAGEN N.V., Myriad RBM, Thermo Fisher Scientific Inc., Athena Diagnostics, Bio-Rad Laboratories, Inc., AbaStar MDx, Inc., Acumen Pharmaceuticals, Banyan Biomarkers, Inc., Alseres Pharmaceuticals, Inc., Proteome Sciences, Immunarray Pvt. Ltd., Quanterix Corporation, Diagenic ASA, and Psynova Neurotech. With increasing digital transformation across industries, the demand for enterprise search solutions is growing significantly to improve information discovery. Major technology players are focusing on artificial intelligence and machine learning integrations to enhance search capabilities. Growing volumes of enterprise data coupled with increasing mobility of workforces is driving the need for powerful search tools within organizations. Enterprise Search Market Trends vendors are developing advanced capabilities for voice search, semantic search and integrated analytics to provide more personalized and contextual results. Technological advancements like natural language processing, deep learning and predictive analytics are enhancing how enterprise search solutions operate to maximize productivity gains. Market Trends The enterprise search market is poised to evolve with two major trends - transition to cloud-based SaaS solutions and integration of advanced analytics. More organizations are opting for cloud-deployed enterprise search as it removes the need for expensive on-premise infrastructure investments and ongoing maintenance. SaaS solutions also enable simpler upgrades and ability to easily scale computing power based on real-time usage. Additionally, vendors are combining enterprise search with advanced analytics to gain actionable insights from organizational data. By identifying patterns and relationships in content, these solutions can offer predictive suggestions along with basic search results. Market Opportunities Growing awareness about improved information discovery and workforce productivity benefits of enterprise search solutions among SMBs presents a major market opportunity. Additionally, integration of enterprise search with unified communication platforms and vertical industry asset repositories also offers scope for enhanced solutions. With continued growth in unstructured enterprise data volumes, development of advanced cognitive capabilities for proprietary language understanding and contextual answers creates new markets. Expanding presence in emerging markets through local partnerships will also fuel next phase of vendor growth. Impact of COVID-19 on Enterprise Search Market The COVID-19 pandemic has significantly impacted the growth of the enterprise search market. During the initial lockdown phase, most offices and workplaces were shut leading to a shift in work models with more employees working remotely. This increased the reliance on digital tools and technologies for collaboration as well as accessing and sharing information across organizations. Enterprise search solutions help employees easily search, access, and retrieve relevant data, documents, and information stored on multiple enterprise platforms from remote locations. This boosted the demand for advanced enterprise search solutions during the pandemic. However, with economic uncertainties and slowing down of businesses due to restrictions and lockdowns, there was reduced IT spending initially in 2020 which impacted the enterprise search market growth negatively. Going forward in 2021 and beyond, as businesses adapt to the new remote and hybrid work models, they will continue investing in digital transformation initiatives and technologies like enterprise search to improve productivity and collaboration. Advanced capabilities like AI/ML integrated search experience, personalization of search results, and integrated search across multiple data sources will be important. North America accounted for the largest share of the enterprise search market in terms of value in 2024. This is attributed to early technology adoption and maturity of enterprise search solutions in this region. However, the Asia Pacific region is expected to grow at the fastest pace during the forecast period owing to increasing digital transformation initiatives, growing internet penetration, and rising focus on customer experience management across industries in countries like China, India. Europe accounted for a significant share of the global enterprise search market in terms of value in 2024. The region has seen large scale deployments of enterprise search solutions across multi-national organizations to help employees easily search and access critical information stored in silos. Many European companies are focusing on personalizing search experiences and integrating AI capabilities like natural language search into their existing enterprise search platforms. Get more insights, On Enterprise Search Market Check more trending articles related to this topic: Cosmetic Botanical Extracts Market The HVAC Equipment Market Will Grow At Highest Pace Owing To Increasing Construction Activities3/19/2024  HVAC Equipment Market The HVAC (heating, ventilation, and air conditioning) equipment market comprises various products such as boilers, chillers, furnaces, heat pumps, packaging units, ventilation units, and others utilized for indoor environmental air conditioning. HVAC equipment are essential components for buildings to maintain thermal comfort and indoor air quality. The rising requirement for temperature and humidity control in commercial, residential and industrial establishments has augmented the demand for HVAC systems. Some key advantages of HVAC systems include maintaining fresh indoor air, controlling temperature and humidity as per requirements, circulating air to improve indoor air quality, removing pollutants, and keeping the surroundings healthy. Growing constructional activities and increasing share of infrastructure projects across developing nations have been instrumental in boosting the HVAC equipment market.

The global HVAC Equipment Market is estimated to be valued at US$ 239.47 Mn in 2024 and is expected to exhibit a CAGR of 7.9% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the HVAC Equipment market are Sterilite Corporation, Rubbermaid, IKEA, KidKraft, Badger Basket, Tot Tutors, Costway, Sauder, Prepac, Honey-Can-Do, Creative Scents, Contico, South Shore Furniture, Seville Classics, Boori, Home Max, Three Posts, Langria, mDesign, Honey Can Do. Major players are focused on new product launches, mergers & acquisitions, investments in research and development activities and strengthening their distribution networks to strengthen their market position. Growing population, increasing disposable incomes, rapid urbanization, and changing preferences towards energy efficient systems have been fueling the demand for HVAC equipment from residential sector. Technological advancements such as development of IoT integrated HVAC systems, sustainable refrigerants, and ductless systems are further propelling the market growth. Market Trends Growing popularity of green buildings - Growing concerns regarding environmental sustainability has significantly boosted the adoption of green building technologies. Green buildings utilize HVAC systems integrated with renewable energy sources and energy efficient components to minimize carbon footprint. Rise of smart HVAC systems - Growing penetration of IoT, automation and integration of AI capabilities have led to the emergence of smart HVAC Equipment Market Trends Smart HVAC equipment can be remotely monitored and controlled through mobile applications, enhance energy efficiency through predictive maintenance and automated operations. Market Opportunities Rising focus on retrofitting of old buildings- Stringent regulations regarding energy usage and ageing building infrastructure in developed nations has augmented retrofitting activities. This presents attractive opportunities for HVAC component suppliers and installers to replace, retrofit or upgrade existing HVAC equipment. Growth in data centers & healthcare facilities - Proliferation of cloud computing, 5G deployment, big data analytics and expansion of healthcare facilities generates substantial demand for specialized HVAC systems to ensure optimal thermal management and air quality in sensitive environments. Impact of COVID-19 on HVAC Equipment Market The COVID-19 pandemic has significantly impacted the growth of the HVAC equipment market. With lockdowns and restrictions imposed worldwide, construction activities slowed down in 2020. This negatively affected the demand for new HVAC systems. Furthermore, supply chain disruptions led to delays and shortages of key components like semiconductors which hampered the production of HVAC equipment. However, with travel restrictions in place, homeowners invested more in home improvement projects which provided some support to HVAC equipment replacement demand. There was also increased focus on indoor air quality amid the spread of the virus which boosted sales of advanced systems with improved filtration capabilities. The commercial sector saw a major decline in new installations due to closure of offices and other establishments. Looking ahead, as vaccination drives progress and economic activities start recovering, construction is expected to pick up pace again. This will drive the demand for HVAC systems in new non-residential buildings. Innovation in remote monitoring and ventilation will remain areas of focus for manufacturers. The priority on health and wellness is likely to sustain interest in premium indoor environment solutions. While short term disruptions are likely if new virus variants emerge, the long term market prospects remain positive with growing awareness around climate control and air quality. Geographical Regions with Highest Value Concentration in HVAC Equipment Market The HVAC equipment market in terms of value is highly concentrated in North America and Europe. North America accounted for the largest share of over 35% of the global HVAC equipment market value in 2024. This was primarily attributed to severe winters in Canada and northern US which drive strong demand for space heating equipment. Moreover, indoor environment quality has emerged as an important factor especially in commercial buildings which has boosted installation of advanced systems. Europe holds the second largest share in the global HVAC equipment market value owing to cold climatic conditions across Eastern Europe and Nordic countries. Strong construction activity accompanied by strict sustainability regulations have also supported market growth in the region. Major countries contributing significantly include Germany, UK and France. Asia Pacific is identified as the fastest growing regional market for HVAC equipment in value terms over the forecast period. Fastest Growing Regional Market for HVAC Equipment Asia Pacific region is projected to be the fastest growing regional market for HVAC equipment during the forecast period of 2024 to 2031. Rapid urbanization and infrastructure development across developing nations such as China and India are major growth drivers. Rising disposable incomes have pushed up demand for energy efficient climate control solutions across both residential and commercial establishments. Government initiatives to promote green buildings using sustainable HVAC technologies also provide impetus. Moreover, growing electronics and automotive manufacturing bases in the region necessitate precise indoor environments which utilizes advanced HVAC systems. Relocation of production facilities from other regions to minimize costs further spurs new installations. The construction of special economic zones and smart cities augment the market expansion. Get more insights, On HVAC Equipment Market Check more trending articles related to this topic: Hashgraph Market  Legal Case Management Software Market The legal case management software market is a solution that helps law firms and legal departments to effectively manage tasks and document workflow. This software helps attorneys efficiently manage their caseload, tasks, court dates and documents. It offers features for document management, billing, time-tracking, calendar management and client communication.

The global legal case management software market is estimated to be valued at US$ 8.3 Mn in 2024 and is expected to exhibit a CAGR of 11% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the legal case management software market are Lumenis, Alma Lasers, THOR Photomedicine, PhotoMedex, Syneron, Galderma, Candela, Beiersdorf, IRIDEX Corporation and Quantel Laser. These players are focusing on developing advanced legal case management solutions and strengthening their distribution networks globally. The growing need to optimize legal workflows and streamline processes is driving the demand for Legal Case Management Software Market Trends The software helps in centralized filing and storage of documents, automated reminders and workflows. This improves efficiency, accountability and reduces costs for law firms. Technological advancements such as AI integration, mobile apps, cloud-based solutions and automation are augmenting the capabilities of legal case management software. AI helps in analytics, classification of documents and automated document generation. Mobile apps allow access to files and management on-the-go. cloud-hosted solutions provide scalability, collaboration and data security. Market Trends Growing adoption of Software-as-a-Service (SaaS) model: Legal case management solution providers are increasingly adopting SaaS or cloud-based subscription model. This provides benefits such as continuous upgrades, remote access, lower upfront costs and reduced IT management. Integration of AI and analytics: Vendors are integrating AI, machine learning and analytics capabilities for automatic categorization of documents, conflict checking, predicting case outcomes and staffing predictions. This is enhancing the productivity and decision making abilities of legal teams. Market Opportunities Emerging markets: Markets in Asia, Middle East and South America are expected to provide significant growth opportunities for legal case management software providers driven by growing legal industry, digitization initiatives and rising internet penetration in these regions. Developing niche software: There is a scope for development of specialized legal case management software for smaller law firms and practices focusing on verticals like immigration law, personal injury, patents etc. This will further drive the adoption. Impact of COVID-19 on Legal Case Management Software Market Growth The COVID-19 pandemic has significantly impacted the growth of the legal case management software market. During the early stages of the pandemic, lockdowns and travel restrictions led to court closures and hearing delays. This reduced the demand for legal case management solutions from law firms and courts.However, as the pandemic progressed, organizations increasingly adopted digital tools and remote working practices to ensure business continuity. This led to renewed demand for legal case management software. Many law firms and legal departments now rely on these solutions to manage case files and collaborate with clients and associates virtually. The shift towards remote legal work is expected to boost the long-term growth prospects of the market. Post-pandemic, organizations are likely to continue supporting flexible and hybrid work models even after offices reopen fully. This will encourage greater adoption of cloud-based legal case management platforms that allow secure remote access. Vendors are enhancing their software with new collaboration features like integrated video conferencing and cloud storage to better support distributed work environments. They are also focusing on cybersecurity to address privacy and data protection concerns arising from remote legal work. Geographical Regions with Major Market Concentration The legal case management software market in North America accounted for the largest share in terms of value in 2024. This can be attributed to early adoption of digital transformation among law firms and courts in countries like the US and Canada. Factors such as stringent data privacy regulations, sophisticated litigation requirements, and tech-savvy legal community have supported technology investments across the North American legal sector. Asia Pacific is projected to be the fastest growing regional market between 2024 to 2030. Countries like China, India, Japan, and Australia are witnessing rising complex litigation and growing emphasis on automation among legal professionals. Increasing digitalization of courts and law firms aims to improve efficiency. Favorable government initiatives are also encouraging adoption of case management solutions in the developing APAC countries. Fastest Growing Regional Market The Asia Pacific region is expected to record the highest CAGR in the global legal case management software market during the forecast period. The rapid economic and digital transformation of countries like India and China is generating more complex commercial litigation. This is fueling the need for advanced software to organize case-related data and documents. Additionally, growing foreign investments into Asia have increased cross-border commercial agreements and disputes requiring tech-enabled legal support. Vendors are also actively partnering with APAC-based system integrators and consulting firms to tap into the opportunities. The positive macroeconomic outlook and supportive government policies make Asia Pacific an attractive emerging market for legal case management solutions. Get more insights, On Legal Case Management Software Market Check more trending articles related to this topic: Hashgraph Market  North America Variable Frequency Drive Market Variable frequency drives (VFDs) are used to control the speed of electric motors, translating input power to variable output power while maintaining motor speed and torque. VFDs help save energy by reducing the motor's speed during low demand periods. They are also used in various industrial sectors like oil & gas, power generation, mining, and others. Advantages include lower operating costs, better process control, lower noise levels, and smoother motor operation.

The Global North America Variable Frequency Drive Market is estimated to be valued at US$ 7240.35 Mn in 2024 and is expected to exhibit a CAGR of 6.6% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the North America Variable Frequency Drive market are Randmark Dental Products, LLC., S4S (UK) Limited, DentCare Dental Lab Pvt.Ltd., Glidewell, Burbank Dental Lab, Brux Night Guard, CUSTMBITE, DDS Lab, Watersedge Dental Laboratory Inc., Orofacial Therapeutics, LP., PFL Healthcare Limited, Keystone Industries, Artistic Dental Laboratories, Inc., Iverson Dental Laboratories, National Dentex Labs (NDX), BonaDent Dental Laboratories, Procter & Gamble. The industrial sector accounts for over 40% market share due to extensive VFD usage in oil & gas, mining, and other industries. Technological advancements are helping improve motor control efficiency and reduce energy usage. Growing demand from renewable energy sector and increasing investments in wind and solar energy will boost North America Variable Frequency Drive Market Demand growth over the forecast period. Technological innovations are leading to development of smarter and more efficient VFDs with enhanced features like integrated safety functions, networking capabilities, and automatic energy savings. Market Trends The oil & gas sector remains the major end user due to widespread VFD deployment in upstream and downstream activities. The rising adoption of electric vehicles is also driving demand as electric motors with VFDs provide efficient power transmission. Increasing investments in renewable energy like solar and wind power generation across North America are boosting VFD market growth. VFDs help optimize motor performance according to fluctuating renewable energy outputs. Market Opportunities Growing emphasis on energy efficiency and conservation worldwide presents significant growth opportunities. Governments providing subsidies for use of VFDs in industrial plants and commercial buildings will further support market expansion. Advancing digitization and automation trends offer an opportunity for development of next-gen smart VFD solutions with integrated sensors, diagnostic tools and connectivity features. Impact of Covid-19 on North America Variable Frequency Drive Market The outbreak of COVID-19 pandemic has significantly impacted the growth of North America variable frequency drive market. During the initial lockdown phases, the demand from end use industries like oil & gas, mining, power generation, etc declined sharply as their operations were halted. This led to reduced demand for variable frequency drives which are used in various process equipment and machinery across these industries. The supply chain disruptions caused by restrictions on transportation and travel bans also affected the procurement of raw materials for manufacturing VFDs. However, as the lockdowns eased, the end use industries started resuming production with limited capacities and strengthened health & safety protocols. This led to a gradual increase in demand for variable frequency drives from second half of 2020. Also, the rising focus on automation and advanced control systems post COVID has boosted adoption of VFDs. The demand is further expected to rise steadily as production levels continue increasing across different verticals in North America region. Ongoing investments towards modernization and efficiency improvement of existing infrastructure is also supporting market growth. Geographical Concentration of North America Variable Frequency Drive Market In terms of value, United States accounts for the major share of over 60% in the North America variable frequency drive market. This is attributed to presence of large process manufacturing sector, robust infrastructure, and high emphasis on industrialization and automation. Canada holds second position with around 25% share and is witnessing fastest growth in the region primarily due to increasing oil & gas projects and rising investments in mining industry. Mexico is emerging as another lucrative market driven by development of automotive industry, power sector expansion, and government initiatives to strengthen manufacturing sector. Fastest Growing Regional Market for North America Variable Frequency Drive Canada is expected to be the fastest growing regional market for variable frequency drives in North America between 2024-2031. This growth can be attributed to factors like recovery of oil prices allowing resumption of stalled energy sector projects, increasing investments in renewable energy infrastructure, and expansion of mining activities. Furthermore, government schemes promoting adoption of energy efficient technologies across industries is creating conducive environment for VFD market growth in Canada. Ongoing modernization of existing plants and rising automation trends will continue driving demand from key end use industries over the forecast period. Get more insights, On North America Variable Frequency Drive Market Check more trending articles related to this topic: Hashgraph Market  Semiconductor Equipment Market The semiconductor equipment market consists of various tools and devices required for manufacturing integrated circuits, semiconductors, and other components. Some key products include lithography systems, wafer processing equipment, metrology systems, and crystal growing systems. There is growing demand for advanced semiconductor devices across various industries like electronics, automotive, healthcare, and telecommunications. Miniaturization of devices and the need for improved performance is driving semiconductor manufacturers to invest in newer fabrication technologies.

The global semiconductor equipment market is estimated to be valued at US$ 95.97 billion in 2024 and is expected to exhibit a CAGR of 12% over the forecast period of 2024 to 2031. Key Takeaways Key players operating in the Semiconductor Equipment are Northrop Grumman Corporation, BAE Systems, Lockheed Martin Corporation, Clearpath Robotics Inc., John Bean Technologies Corporation, ECA Group, Israel Aerospace Industries Ltd., Endeavor (Now a part of FLIR system), Harris Corporation, and General Dynamics. The demand for semiconductor devices is growing exponentially due to proliferation of consumer electronics and adoption of IoT. This is prompting equipment manufacturers to develop more advanced lithography, deposition, etching, and metrology tools. Major technology trends include EUV lithography, advanced packaging, and metrology solutions based on machine learning. Market Trends Miniaturization of semiconductor devices is a key trend as it allows for development of smaller and powerful electronics. This is driving the need for newer lithography technologies like EUV with higher resolution. Another major trend is the shift towards packaging technologies like 2.5D and 3D stacking to address issues of processor speed and connectivity. This has increased demand for backend equipment and inspection systems. Market Opportunities Growing applications of Semiconductor Equipment Market Demand in automotive, healthcare and other industries present significant opportunities for equipment suppliers. This includes developing tools for new advanced nodes of 5nm and below. There is also scope for equipment manufacturers to offer integrated solutions combining multiple process steps rather than standalone tools. Developing MEMS fabrication equipment for niche applications like sensors can unlock new growth opportunities. Impact of COVID-19 on Semiconductor Equipment Market Growth The COVID-19 pandemic severely impacted the semiconductor equipment market growth globally. During the initial outbreak, manufacturing activities were halted as lockdowns were imposed across major economies. This led to disruptions in the supply chain and demand decline. Component shortages affected the production of chips used in various end-use industries like automotive, consumer electronics, etc. However, as lockdowns were relaxed in late 2020, the market started recovering gradually. The pandemic accelerated digital transformation across sectors. Work from home practices increased the demand for laptops, smartphones, networking equipment driving chip requirements. The growth of 5G networks and advancement in technologies like AI, machine learning, IoT also aided market recovery. The increasing demand for semiconductor chips from automotive industry adopted advanced driver-assistance systems and infotainment protocols further supported market growth. To cater to the rising demand, chip manufacturers increased their capital expenditure on advanced manufacturing equipment, lithography systems, metrology devices. The supply chain stabilized as logistical constraints were addressed. Several governments announced incentives to boost local chip manufacturing attracting new wafer fabrication facilities. The semiconductor equipment market is poised to grow further in the coming years driven by increased investments in advanced technologies, new applications, and regional self-sufficiency programs. Geographical Regions with High Semiconductor Equipment Market Value Asia Pacific dominated the market in terms of value, accounting for over 50% share owing to the presence of leading wafer fabrication hubs in countries like Taiwan, South Korea, China, and Japan. Majority of global foundries, IDMs, and OSAT companies have their manufacturing facilities in the region to cater to rising regional chip demand. The increasing number of fabs along with capacity expansions are driving equipment procurement in APAC. North America is the fastest growing region on account of new fabs commissioned by Intel, TSMC, Samsung, and investments under CHIPS Act. The act aims to catalyze US$52 billion of semiconductor investments and research creating a vibrant domestic supply chain. European Union is also emerging as an important fabrication destination supported by public-private partnerships to boost regional chip self-sufficiency and address the ongoing supply issues. Geographical Region with Fastest Growing Semiconductor Equipment Market North America region is expected to witness the fastest growth in the semiconductor equipment market during the forecast period on account of increasing investments to develop domestic semiconductor manufacturing capabilities. Governments across U.S. and Canada are offering attractive incentives under programs like CHIPS act and Strategic Innovation Fund to attract major OSATs, foundries, and IDMs. Some key factors fueling fastest growth in the North America region include- new MEMS fab commissioned by STMicroelectronics in Syracuse, New York expanding 300mm wafer capacity, Intel's $20 billion investment in Ohio and Arizona fabs, TSMC and Samsung selecting sites in Arizona for new fabs, GlobalFoundries expanding its Malta, New York fab and investments from ON Semiconductor and SkyWater Technology. The growth of 5G/6G infrastructure and adoption of EVs are also driving regional chip demand supporting equipment procurement. Get more insights, On Semiconductor Equipment Market Check more trending articles related to this topic: Soda Ash Market  Wave Energy Converter Market The wave energy converter market involves the capture of kinetic and potential energy from ocean surface waves to generate electricity. Wave energy converters use wave motion to power water turbines or pump hydraulics to drive electrical generators. They offer advantages such as low environmental impact, predictable output, and nearly limitless fuel source. Governments across the globe are promoting renewable energy sources to reduce dependence on fossil fuels and mitigate climate change risks. Growing focus on the development of ocean energy resources presents a key opportunity for the wave energy converter market. The global wave energy converter market is estimated to be valued at US$ 19.52 billion in 2024 and is expected to exhibit a CAGR of 4.2% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the wave energy converter market include Ocean Power Technologies, Marine Power Systems, Eco Wave Power, SINN Power GmbH, NEMOS GmbH, INGINE Inc., Carnegie Clean Energy, CorPower Ocean, AW-Energy Oy, AWS Ocean Energy, Wello Oy, HavKraft AS, Wave Dragon, Wave Swell, and Aquanet Power. Ocean Power Technologies and Marine Power Systems currently lead the market with their array of wave energy converter products. Wave Energy Converter Market Trends Growing environmental concerns and policy support for renewable energy have led to a surge in demand for wave energy technologies in recent years. Countries with high wave energy potential such as the UK, Portugal, and Australia are investing heavily in wave farms and pilot projects. Advancements in materials, power take-off systems, and mooring technologies have improved the efficiency and durability of wave energy converters. Developers are working on next-generation concepts such as oscillating water columns and overtopping devices to optimize wave energy extraction. Market Trends Increasing investments in offshore renewable energy - Several governments are implementing fiscal incentives and tenders to encourage the commercialization of offshore wind and wave energy projects. This is expected to boost investments in wave energy converters. Focus on development of utility-scale wave farms - Major players are collaborating to develop multi-MW wave farms through innovative floating converter designs and optimized mooring systems. Utility-scale deployment holds potential to achieve grid parity for wave energy. Market Opportunities Growing interest from remote communities and islands - Islands and coastal regions dependent on imported diesel for electricity see wave energy as a means to transition to indigenous renewable sources. This presents an opportunity for small and modular wave energy systems. Integration with existing infrastructure - Developers are exploring ways to leverage existing offshore oil & gas platforms and pipelines to reduce costs associated with wave energy projects. Such integrated solutions could expedite the adoption of wave energy converters. Wave Energy Converter Market Impact of COVID-19 COVID-19 pandemic has significantly impacted the growth of wave energy converter market. The stringent lockdowns imposed across various countries led to temporary suspension of manufacturing facilities. This significantly disrupted the supply chain and logistics for raw materials procurement and product distribution. Furthermore, travel restrictions impacted installation and commissioning of new wave energy projects. This led to delays in project timelines during 2020 and 2021. However, growing focus on renewable energy and need to reduce dependence on fossil fuels is expected to drive investments in wave energy post-pandemic. Government incentives and subsidies are focusing on renewable sector to aid economic recovery. Initiatives such as Build Back Better plan in US are expected to boost investments in offshore renewable energy projects including wave energy in coming years. Accelerated digital transformation during pandemic has paved way for remote monitoring solutions for wave farms. This is likely to reduce O&M costs and facilitate quicker commissioning of new systems. Geographical Regions where market is concentrated Europe accounts for more than 50% of global wave energy converter installations in terms of value as of 2024. Countries such as UK, Portugal, Spain, Ireland and Norway are early adopters of wave energy technology and have built commercial wave farms. Government support through incentives, permitting streamlining and funding has propelled the growth of emerging sector in these countries. Asia Pacific region is expected to grow at fastest pace, driven by investments in South Korea, China and Australia. Incentives supporting Wave Energy research in countries like Australia, Chile and US west coast are attracting device developers and private capital to these regions. Fastest Growing Region Asia Pacific region is projected to witness highest CAGR in wave energy converter market during forecast years of 2024 to 2031. Countries like South Korea, China, Philippines, Vietnam, Indonesia etc. offer large untapped market potential propelled by growing investments in offshore renewable sector. Rising demand for clean energy, supportive government policies through incentives and targets for renewable ocean energy are driving the growth. Initiatives such as Japan's 5th Strategic Energy Plan aiming to derive 1 GW of power from ocean energy by 2030 are likely to boost technology deployment in APAC. Developing economies are witnessing rising number of pilot wave energy projects with private sector participation. Advent of new device designs suitable for local wave climates and investments in smart grid infrastructure are factors expected to accelerate the market growth in Asia Pacific. Get more insights, On Wave Energy Converter Market Check more trending articles related to this topic: Soda Ash Market  Embedded FPGA Market In the realm of electronics and digital systems, Embedded Field-Programmable Gate Arrays (FPGAs) have emerged as versatile solutions, offering unparalleled flexibility and performance. As the demand for customization and adaptability continues to soar across industries, exploring the evolving trends and demand drivers in the global embedded FPGA market becomes imperative. Let's delve deeper into the opportunities awaiting exploration in this dynamic landscape.

Global embedded FPGA market is estimated to be valued at USD 109.82 million in 2024 and is expected to reach USD 302.96 million by 2031, exhibiting a compound annual growth rate (CAGR) of 15.6% from 2024 to 2031. Rising Demand for Customization: One of the primary drivers propelling the demand for embedded FPGAs is the need for customization. In an era where off-the-shelf solutions often fall short of meeting unique requirements, FPGAs offer the flexibility to tailor designs to specific applications, thereby unlocking new possibilities in diverse domains, including aerospace, automotive, telecommunications, and more. Accelerated Time-to-Market: In today's fast-paced market environment, time-to-market can make or break a product's success. Embedded FPGAs enable rapid prototyping, iteration, and validation, empowering designers to expedite development cycles and seize market opportunities ahead of competitors. This agility is particularly crucial in industries characterized by rapid technological advancements and evolving customer preferences. Proliferation of IoT Devices: The Internet of Things (IoT) revolution is driving unprecedented demand for Embedded FPGA Market Trends as connected devices require robust yet adaptable hardware platforms. FPGAs offer the versatility to accommodate diverse communication protocols, sensor interfaces, and processing capabilities, making them indispensable components in IoT edge devices, smart sensors, and industrial automation systems. Edge Computing and AI Acceleration: As edge computing gains traction, embedded FPGAs are poised to play a pivotal role in enabling real-time processing and analysis of data at the network edge. Moreover, FPGAs offer inherent parallelism and reconfigurability ideal for accelerating artificial intelligence (AI) workloads, including machine learning inference, computer vision, and natural language processing, unlocking new frontiers in intelligent edge devices. Security and Reliability Imperatives: In safety-critical applications such as automotive electronics, industrial control systems, and medical devices, security and reliability are paramount. Embedded FPGAs offer built-in security features, such as hardware root of trust, secure boot, and cryptographic acceleration, bolstering defenses against cyber threats and ensuring system integrity in mission-critical environments. Ecosystem Collaboration and Innovation: The embedded FPGA market thrives on collaboration between FPGA vendors, semiconductor manufacturers, and ecosystem partners. By fostering open standards, developer communities, and ecosystem support, stakeholders can drive innovation, accelerate adoption, and unlock synergies that fuel market growth and differentiation. In summary, the global embedded FPGA market presents a myriad of opportunities for innovation and value creation across industries. By embracing customization, accelerating time-to-market, harnessing the power of IoT and edge computing, and prioritizing security and reliability, businesses can unlock the full potential of embedded FPGAs and stay ahead in today's competitive landscape. As technology continues to evolve, the journey of exploration and discovery in the embedded FPGA market promises to be both exciting and rewarding.  Hybrid Cells The field of cell biology is continuously evolving with new groundbreaking discoveries that are helping scientists better understand how cells function. One such major development is the emergence of hybrid cells that combine the properties of different cell types. Hybrid cells offer tremendous potential in both research and therapeutic applications. In this article, we explore what hybrid cells are, how they are created, and their potential role in advancing medical science.

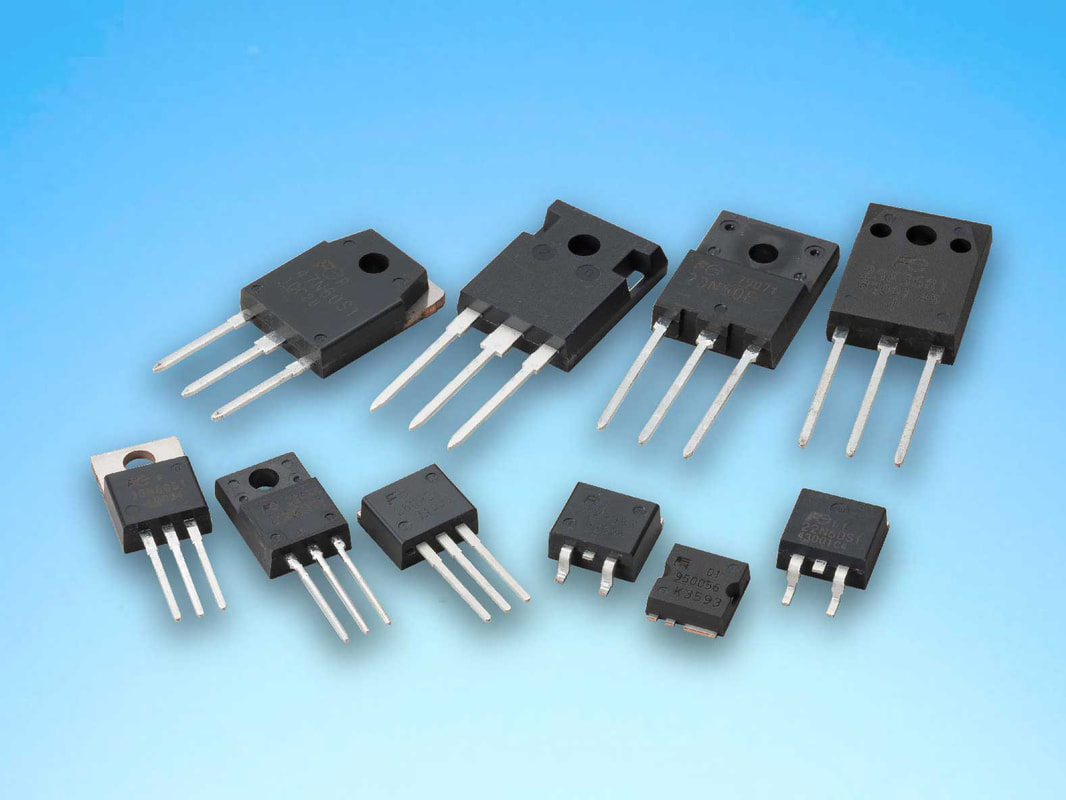

What are Hybrid Cells? Hybrid cells, also known as cell hybrids, are artificial cells created by fusing two or more different eukaryotic cell types using cell fusion techniques. The resulting hybrid cell contains a combination of genetic material from the parent cells. Through cell fusion, researchers can combine desirable traits from different cell lines to study gene interactions and functions. Some key characteristics of hybrid cells include: - They contain a mixed genome from two or more original cell types - They exhibit properties of both parent cell types - Researchers can use them to study crossed traits and gene interactions Methods of Creating Hybrid Cells There are a few main techniques scientists employ to create hybrid cells in the laboratory: Chemical-induced Cell Fusion One of the most common methods involves chemically Hybrid Cell fusion using chemicals like polyethylene glycol (PEG). PEG works by dehydrating the outer cell membranes of two different cells, causing them to fuse together forming a single hybrid cell containing genetic material from both parents. Electrofusion This technique utilizes short pulses of electric currents to physically destabilize the outer cell membranes and fuse adjacent cells together. Electroporation creates temporary pores in the membranes through which the intracellular contents can mix resulting in hybrid cell formation. Viral-mediated Cell Fusion Some viruses like the sendai virus have glycoproteins on their envelope that assist in fusing host cell membranes during viral entry. Researchers leverage this property of viruses by incubating two cell types with inactivated sendai virus to induce fusion between adjacent cells at the contact points. Applications of Hybrid Cells in Research Hybrid cells provide unique opportunities for studying complex biological questions. Some key areas where hybrid cell research is contributing include: Gene Mapping By assessing the traits exhibited by hybrid cells, scientists can map the inheritance of genes and identify their locations on chromosomes. This assists in characterizing gene functions and interactions. Organelle Inheritance Studying hybrids derived from cell types with distinct organelles like mitochondria helps uncover mechanisms of organelle transmission during cell division. Oncogene Expression Fusion of cancer cells with non-cancerous cells is helping delineate specific genes responsible for cellular transformation and tumor formation. Stem Cell Plasticity Creating hybrids between stem cells and differentiated cell types provides insights into epithelial-mesenchymal transition, a process tied to development and disease. Potential Medical Applications Beyond research applications, hybrid cells hold therapeutic promise in a variety of areas like regenerative medicine and cancer immunotherapy: Tissue Engineering Stem cell hybrids exhibiting characteristics of multiple lineages could be useful for engineering complex tissues like bone, cartilage and vasculature for transplantation purposes. Cell-based Vaccines Hybrids generated by fusing dendritic cells to tumor cells may serve as off-the-shelf vaccines by triggering anti-tumor immune responses within the body. Enzyme Replacement Therapy Leveraging hybrids between patients' cells and enzyme-producing donor cells could help treat genetic disorders caused by enzyme deficiencies. Overcoming Transplant Rejections By fusing transplant recipient’s cells with donor organ cells, scientists aim to synthesize tolerated grafts not targeted by the recipient’s immune system. Concluding Remarks In summary, hybrid cells represent an area of tremendous opportunity at the intersection of cell biology and biomedical technologies. Through a better understanding of their fundamental properties and behaviors, hybrid cell research is advancing basic science while also fueling innovative therapeutic modalities. With further refinements in cell fusion methodology, hybrid cell applications are expected to grow in scope and help address many unmet medical needs. Get more insights, On Hybrid Cells  IGBT And Super Junction MOSFET Market IGBT (Insulated Gate Bipolar Transistor) and Super Junction MOSFET are power semiconductor devices that are widely used in automotive electronics such as engine control modules, battery management systems, and electric vehicle motor drive applications owing to their low turn-on and turn-off times and low conduction losses. These devices are used as switches in circuits that require high efficiency, fast switching and ability to handle large voltages and currents. The global automotive industry is witnessing significant growth with rising vehicle production and increasing integration of electronic components in vehicles. With governments worldwide pushing for electrification of transportation systems, the demand for IGBTs and MOSFETs is expected to surge significantly in the coming years.

The Global IGBT and Super Junction MOSFET Market is estimated to be valued at US$ 18637.33 Mn in 2024 and is expected to exhibit a CAGR of 5.1% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the IGBT and Super Junction MOSFET market are Pfizer Inc. (U.S.), ARGON MEDICAL (U.S.), Edwards Lifesciences Corporation (U.S.), BD (U.S.), Alcaliber S.A. (Spain), Lupin Pharmaceuticals, Inc. (India), Vitaltec Corporation (China), Medtronic (U.S.), Koninklijke Philips N.V. (The Netherlands), Siemens Healthcare GmbH (Germany), Hitachi Medical Corporation (U.S.), and Canon Medical Systems Corporation (Japan). The growing demand for IGBTs from the electric vehicle industry is a major factor boosting the market growth. With advancements in wide bandgap materials like silicon carbide (SiC) and gallium nitride (GaN), power semiconductors can switch at even higher frequencies with lower power losses, making them ideal for high-efficiency power conversion applications. Market trends: 1. Wide bandgap materials: GaN and SiC based IGBTs and MOSFETs offer significantly lower conduction and switching losses compared to their silicon counterparts due to their wide bandgaps and higher breakdown field strengths. This makes them suitable for applications requiring high switching frequencies and high operating temperatures. 2. Integration of power semiconductors: Monolithic integration of power devices, control ICs and gate drivers on a single chip reduces parasitics and enables miniaturization of power modules. Integrated devices cater to the demand for compact and efficient power electronic systems. Market Opportunities: 1. Electric vehicles: Rapid growth of the worldwide EV market presents lucrative opportunities for power semiconductor manufacturers. IGBTs and MOSFETs have a major role to play in electric drivetrains, on-board chargers and battery management systems. 2. Renewable energy systems: Power devices are critical components in solar and wind energy conversion equipment. Their demand is expected to steadily rise in line with increasing focus on alternative and clean energy sources. Impact of COVID-19 on IGBT And Super Junction MOSFET Market Demand Growth The COVID-19 pandemic has adversely impacted the growth of the IGBT and Super Junction MOSFET market. Stringent lockdowns and restrictions on travel and transportation enforced by governments globally disrupted supply chains. This led to reduced availability of raw materials for manufacturers. Further, with employees working from home, the demand for electronic devices from consumers decreased significantly in 2020. The pandemic also postponed or cancelled investments in automotive, industrial and renewable energy projects which are major end-users of IGBT and MOSFET components. However, with mass vaccination drives and relaxation of COVID norms from 2021, the supply chains resumed operations and new orders flowed in. Many technologies related to medical devices, communication infrastructure, data centers also saw increased demand which boosted the market. Nevertheless, the market is yet to fully recover from the economic damages of 2020. Regions with Concentration of IGBT and Super Junction MOSFET Market Value In terms of value, the IGBT and Super Junction MOSFET market is most concentrated in Asia Pacific region particularly in countries like China, Japan, South Korea and India. These countries are global hubs for electronics and automotive production. They account for over 60% of the global demand for power semiconductors used in devices, equipment and vehicles manufactured in the region for domestic as well as export markets. North America and Europe are other major regional markets led by the US, Germany respectively due to establishment of automotive OEMs and presence of ancillary industries. Fastest Growing Region in IGBT and Super Junction MOSFET Market Currently, the fastest growing regional market for IGBT and Super Junction MOSFET is South East Asia led by countries like Indonesia, Vietnam, Philippines and Thailand. This is due to rising electronics exports, entry of global automakers in local production and focus of governments on developing renewable energy sectors in these nations. South East Asia is witnessing exponential economic growth backed by rising incomes, growing youth population and increasing foreign investments. Due to availability of cheap labor and resources, many electronic and components manufacturing units are being set up in the region propelling the power semiconductor demand upwards in the coming years. Get more insights, On IGBT and Super Junction MOSFET Market |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

February 2024

Categories

All

|

RSS Feed

RSS Feed